Deconsolidating losses.

The Micro Investor #7

Good morning Micro Investors!

Welcome to a new edition of Micro Caps in 10 minutes. If you are not yet subscribed, you can join the best newsletter for independent investors who are not afraid to invest in the most unknown companies in the market. If you are a colonizer of the micro cap universe, this is your place.

Today in 10 minutes:

1 - Quick pitch: Tenderhut (WSE:THG)

2 - HAV Group (OSL:HAV) gets another contract.

3 - More things from Twitter.

Quick pitch: Tenderhut

I would like to thank the following twitter user, from whom I’ve got the THG idea: https://twitter.com/safe_our_souls

Totally worth it to follow if interested in polish stocks.

Tenderhut (WSE:THG) is a profitable business that has grown its profits at a 37% CAGR in the last 5 years, these profits are being masked by various side start up businesses that still lose money. The board of directors has raised several rounds of financing and intends to list some of these businesses, which would bring out this hidden value, both in the income statement (eliminating losses) and in the balance sheet (transforming part of the value into cash).

I think Tenderhut is an investment with a very good chance of generating returns in excess of 20% per year because the value of their side businesses is 50% of capitalization, and we're buying the core business for 5-8x profit.

Shares of tenderhut are down from the IPO price in ‘21.

Description

TenderHut is a Polish software company dedicated to providing IT integration and programming services for small and medium businesses. Its sales have grown at 36% CAGR in the last 5 years, while EBIT has grown at 37% CAGR. It is trading at PLN 86m and an EV of PLN 77m. In '22 it had sales of 77.7M PLN, net profits of approximately 5.5M PLN, trading at P/E 14 excluding cash.

These gains, however, include losses from several consolidated companies on the balance sheet that are still developing their digital products. Those are start ups that operate independently from the main business and have already raised financing rounds, so the effect on the main business will be limited in the future and they must be assessed independently.

Let me explain, I promise you that no adjusted EBITDA or black magic needed.

Structure

To better understand this, let's see how the company is structured and make a valuation by parts. Its services are organized in:

Programming services, UI design for applications and digital marketing (74%)

Software integration services from the provider "Thermo Fisher" in laboratories. (16%).

Other businesses in development, start-ups. (10%)

In point 3 lies the gap between the optical valuation of TenderHut and the real one. TenderHut consolidates on its balance sheet these companies:

Holo4Labs Sp. z.o.o - Virtual reality systems for laboratories based on Microsoft HoloLens.

Holo4Med Sp. z.o.o - Similar to the previous one but aimed at hospitals.

Grow Uperion Sp. z.o.o - Apps for employee motivation transforming daily tasks into games.

Zonifero, Sp. z.o.o - App for digital office management, allowing you to book rooms or find co-workers in real time.

All these products are in very early phases, they barely generate revenue and do generate losses. In '22, between all of them they had 7M PLN revenue and 6.8M PLN of losses (data annualized as of Q3 '22).These losses dwarf the profits of the core business.

Stripping out these losses, core businesses have delivered a 10.5% net margin in '21. PLN 6.4M profit.

Giving a valuation to these startups is not complicated, fortunately all of them have received rounds of investment, both through crowdfunding and from institutional investors.

THG's shares in its other businesses are worth PLN 46m based on the latest investor valuation.This would leave the core business trading at PLN 31m or 4.2 P/E.

This value is not shown on the balance sheet because they are consolidated, it will surface in the event that they begin to trade or are sold. THG's board of directors has expressed its intention to list Holo4Med and Zonifero, although they may delay it given the current market situation.

Even taking this valuation as excessive (which is perfectly possible considering the frenzy of '20 and '21) and reducing it by 50% would leave us with an EV of 54M and a P/E of 7.3

In my opinion, too little for a business that grows at more than 30% per year.

But, we still have to analyze the acquisitions, the directive, the sector, and some valuation scenarios.

All of this in the next edition of Micro Caps in 10 minutes.

Here I leave the button to subscribe if you do not want to miss it (and if you want to make me very happy)

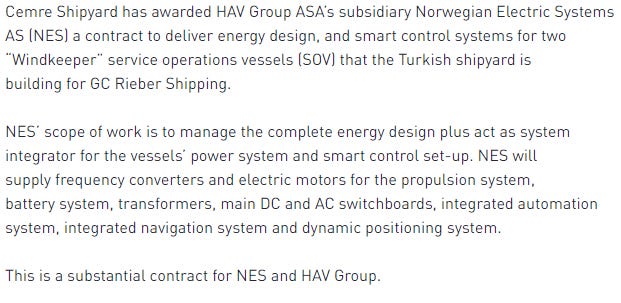

In portfolio: HAV receives a new contract

In the last edition of this newsletter I told you that HAV Group had won two new contracts...

Well, they have received another one, for two boats:

Between all these contracts we could have between 200-300M NOK of extra backlog, a good step to get closer to the sales of '21, which would leave the company trading at 3x EBIT.

The stock is up 20% since then.

From Twitter

Another very well structured thesis from GEE Group (NASDAQ:JOB). Totally recommended.

Sebastian post about special situation. I’m very interested in the Centrotec case.

Chinese Nano Cap that manufactures supplies and consumables for travel, trading at P/E 3, a 10% dividend and with an activist investor.

Some memes about Chinese balloons.

And that’s a wrap for today! Hope you enjoyed.

See you in the next edition of Micro Caps in 10 minutes.

Dani