The Sun Factory (plus others)

Micro Caps in 10 minutes #4

Good morning Micro Investors!

Welcome to Micro Caps in 10 minutes. If you are not yet subscribed, you can join the best newsletter for independent investors who are not afraid to invest in the most unknown companies in the market. If you are a colonizer of the micro cap universe, this is your site.

In this new section, which I will publish every 2 Fridays, we will review updates on the companies in the portfolio, news and investment (or non-investment) ideas. With this I will try to publish content in a consistent way without limiting the newsletter to only long company reviews.

Today in 10 minutes:

1 - Idea: Gibus. The Sun Factory

2 - Future research: Redishred and Laser Photonics Corporation

Idea: Gibus. The Sun Factory

Gibus is an Italian manufacturer of high end pergolas, awnings and blinds. Its flagship product is the bioclimatic pergola, which has mobile sheets on the roof that open and close at variable angles and allow the amount of sun that passes into the pergola to be regulated. In addition to this they are remotely controllable and have extras such as lights or solar panels.

These are luxury products, while a 400x300cm pergola at the general distributor Leroy Merlin costs about €3,900 (as of December '22) a pergola bioclimatic Gibus of the same size costs about €14,000.

These prices translate into good margins, with a gross margin of 40% and operating margin above 20%. It's not like it's a very capital intensive company either, to achieve an EBIT of €16M in '21 they only needed €40M in assets excluding cash. And the cash, which is 30% of the market cap, is not necessary for the development of the business because the working capital is almost zero (even negative some years). This makes sense because much of their products are custom-built, making them to order and charging them earlier than they pay their suppliers.

If we exclude cash we have a ROCE above 100%. I certainly don't expect them to be able to sustain this as they scale and it probably wouldn't be wise to take all the cash out of the business either, but the point is that at first glance it it's a very quality business.

The founder of Gibus, Gianluca Belli is still active as president of the company and controls 80% of the shares, he is aligned with the shareholder.

And this business is trading at 3 times EV/EBITDA and a P/E of 5.

Why is it so cheap?

Gibus has been benefiting from a very important tailwind in the last 2 years.

The ecobonus

As part of the economic measures to reactivate the economy after the coronavirus pandemic, the Italian government introduced the "Relaunch Decree" in mid ‘20 with a series of fiscal stimuli. One of them is the Ecobonus.

The Ecobonus consists of discounts on the payment of taxes when buying items to improve energy efficiency or reform exteriors in homes and businesses. The grant comes in a version that deducts 110% of the value of the reform for a few eligible cases and a more general version that deducts 50%. The latter is the one that applies to Gibus products.

Although the aid is designed so that the beneficiaries discount the subsidized amount in the tax payments of several years after the reform, the discount can be sold. With this, what is achieved is that these "credits" are purchased by banks, and an effective discount of 50% (less interest) can be obtained on the purchase invoice.

Overnight, Gibus products cost half to its customers. This has generated a boost in demand and Gibus sales in Italy grew by 74% in 2021.

And best part.

The ecobonus, which was going to last until the end of ‘21, has been extended until December ‘24.

Sales in Italy continue to grow in ‘22 and in the first half of the year they have registered sales 34% higher than in ‘21. All this growth is partly thanks to post-covid outdoor boom , partly expansion to a customer market that could not afford Gibus luxury products, and mostly anticipated demand. If the bond has a limited time, clients who are thinking of renovating their exteriors do so now and not in a few years.

The party is going to end and we will have a good hangover, at least that is what should happen to justify the current valuation in a quality business like Gibus's.

Pergolas and awnings market

The Allied Market Research agency has published this study, in which it quantifies the current market for pergolas and awnings in Europe at €2.1B in ‘19, with an expected growth of 3.9% CAGR until ‘27. Moderate growth, somewhat above that of GDP, as might be expected.

What I find most interesting is that the main competitors in this market are mentioned in the study summary, which are: Commercial Awnings Limited, Gibus, Markilux Gmbh, Marquises, MHZ Hachtel Gmbh & Co. KG, Mitjavila, Shades-Awnings, Varisol , Warema Renkhoff Se, and Weinor.

It seems that Gibus, with sales of €35M in ‘19, is among the main competitors in a €2B market, with a market share of 1.7%. The rest of the competitors are not listed, but we can get an idea of their size based on the number of employees.

For reference, Gibus has 260 employees.

Commercial Awnings Limited - Does not show it on Linkedin, other reports show less than 10.

Weinor - 59 employees on Linkedin.

Warema - 424 employees on linkedin.

MHZ Hachtel GmbH & Co. KG - 170 employees at linkedin.

MARQUISES STORES - 8 employees on linkedin.

Markilux GmbH + Co. KG - 109 employees on linkedin

If Gibus with €80M in sales in ‘22 has 260 employees, Warema, the largest of the competitors could be in the range of €100M - €150M, 6% of the share market. In fact, among all the competitors mentioned in this report, they would be somewhat above 10% of the market share.

This means that the market is highly fragmented and most competitors in the market will be in the €1M - €10M sales range.

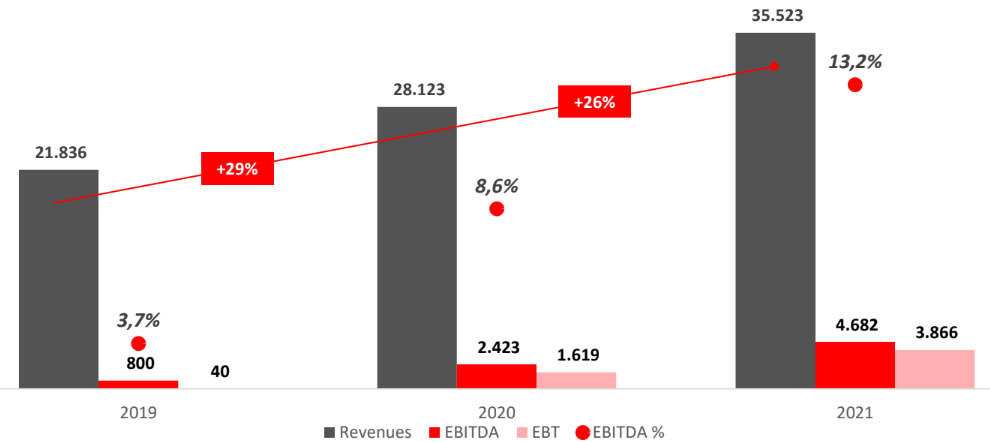

Operating leverage

These are the sales, gross margin, operating margin, and net profit of Gibus from ‘17 to 2022. I know there are a lot of things in one graph, take a minute to look at it.

Gross margin has remained almost constant. The operating margin has increased from 10% to 20%. Profits have multiplied by more than 6 when sales have multiplied by 2.

Operating leverage? It definitely seems that way.

Overheads from 2017 to 2021 have only gone up 50% when production has doubled. It's quite possible that most of this operating leverage has already been captured with sales growth in recent years and we shouldn't expect margins to go much higher, but operating leverage seems very important to me for another reason. M&A

Expansion and diversification

So, Gibus has benefited greatly in the last two years from the ecobonus, which basically subsidizes half the sale price of its products and from the post-pandemic outdoor living boom. Being a business with a very high ROCE, it is not that they need to invest too much to grow, so from having €5M in cash at the end of ‘19 they have gone to €24M at the end of ‘21.

On the other hand, Being a company with such high growth in sales due to external factors and operating leverage, the greatest risk is contraction in ‘25, when the ecobonus ends.

Operating leverage works both ways and if sales drop 50% profits can drop 80%.

It is reasonable for the company to use the cash it has now to go in one direction: to increase its sales outside of Italy.

And that's what it did a couple of months ago, buying Leiner, one of its German competitors:

The share price has reacted well to this purchase, I think because of what I just mentioned, if when sales in Italy drop in ‘25 the company is still large enough the impact on margins will be less.

The acquisition of Leiner

The purchase price of Leiner has been €31.6M, if we add to this the €5.2M debt that Leiner has with its previous owners, the total amounts to €36.8M. Leiner's pre-tax profits in 2021 have been €3.9M.

At 9.4 times EBT, the acquisition has not been cheap.

However, again, operating leverage. Leiner's EBITDA margin in ‘21 was 13% with €35M in sales. GIBUS, in ‘18 with €34M in sales, also had an EBITDA margin of 12.7% and this margin has grown to 25% in ‘21, only gaining scale.

The two businesses seem very similar and possibly the Gibus - Leiner synergies have the same result, so we are buying at about 5 times EBT. That would be much more reasonable.

What will happen in 2025

Sales within Italy have grown by 75% in ‘21 and 36% in ‘22, compared to 23% and 4% outside. Gibus, thanks to the ecobonus, is possibly anticipating demand for subsequent years and accessing customers who would otherwise opt for a cheaper product.

It is difficult to know the effect that the end of the bonus will have in ‘25, to be conservative I will assume that sales in Italy return to the same level as in ‘20, sales abroad in Italy grow at 15% per year, below 25% per year. which grew until ‘21.

We would end ‘25 with sales of €100M, similar to what they will have this year including the acquisition of Leiner. Gibus trades at 5 times earnings.

And until ‘25 it is likely that sales in Italy will continue to grow thanks to the ecobonus, so excluding cash we could find ourselves in ‘25 trading at 2 times earnings.

Conclusion

Gibus meets all the requirements to generate good long-term returns and should not trade at a multiple of a semi-commodity industrial company. It is true that it has tailwinds because of the subsidies in Italy, but these winds are still going to help us for another couple of years, and we are very protected by the low valuation. In the meantime we have the opportunity to grow organically at 10-20% with almost no investment required and use the cash for acquisitions.

What am I going to do

Gibus remains as the number 1 candidate to add to the portfolio, I am not going to sell any of my positions because I think they have similar potential, but at some point we will have to diversify.

Anyway, I prefer to analyze first other ideas with potential such as:

Future research

Redishred (KUT): Sensitive documents shredding

Laser Photonics Corporation (LASE): Special situation

If you don’t want to miss out on illiquid and market overlooked companies remember to subscribe to The Micro Investor Newsletter